The M&G and PET Reality Show...What Could Have Been.

Essay by John C. Maddox, CEO of SBAcci

If this was a reality TV show, Guido Ghisolfi’s death in 2015 could have been viewed as the beginning of the end, the breaking point. But this was REAL reality, and the M&G PET plant in Corpus Christi, Texas was well beyond the design and engineering phase by the date of Guido’s untimely passing. Furthermore, Guido was not the only person at M&G with adequate technical skills. Others stepped up and filled in quite nicely. Besides, the Corpus Christi plant did not feature much ground-breaking new technology. Sure, it was larger in scale and had some improvements in terms of the SSP units, but nothing overwhelming. Corpus Christi was the third plant – after Recife (Brazil) and Altamira (Mexico) – to implement a scaled-up version of the company’s Easy-up® PET design technology. Beautiful technology. Proven. Offering flexible formula changes without stopping or transitioning melt with M&G’s innovative BicoPETTM and the IV flexibility of two SSPs being fed by one huge melt phase unit.

Aside from making some great memories with Guido at social events and a few business meetings, I cannot claim to have known him well. I arbitrated negotiations between him and an M&G business partner once. The resulting compromise proved that he was tough, but fair. He was universally respected around the world for his technical skills and business acumen. His death is a huge loss for the industry – but of course, nothing like the loss to his family.

Back to reality. Just 90 more days ... if there had been just 90 more days of all-out construction activity at Corpus Christi, the PET portion of the world’s largest single-train PET plant could have been realized. With production, there would have been cash flow. And with cash flow, there would have been happy vendors and suppliers. And with raw material supplies, there would have been happy customers and happy creditors. So close. After about one billion dollars spent, it was just SO close.

But where did it all begin? What were the long-term industry drivers? What changed, and why? When did it begin falling

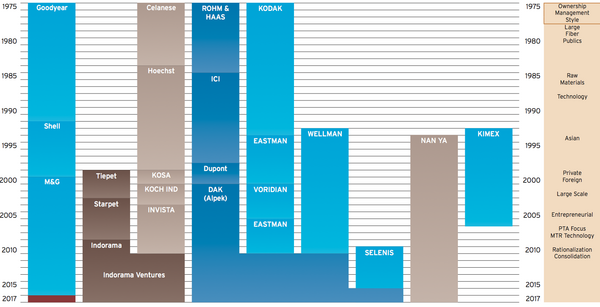

apart? And not for just M&G. Long before M&G, there was Kimex; there was Wellman’s bankruptcy in 2010; there was the decision by Koch Industries to sell off Invista to Indorama and Eastman Chemical’s decision to sell their PET assets to DAK. More recently Selenis Canada sold its controlling interest to DAK. Before 2010 there were nine PET resin producers in NAFTA; now, if M&G vanishes, only three marketers of PET resin (DAK, Indorama and NanYa) will remain. And these are just the transitions in North America. Europe has seen similar mergers, acquisitions, up-stream buys, down-stream buys, business failures and even incarcerations. Asia, with its massive build-up of not only PET resin but also PET raw materials, is sure to be next. The older, smaller, non-vertically integrated plants are already in trouble.

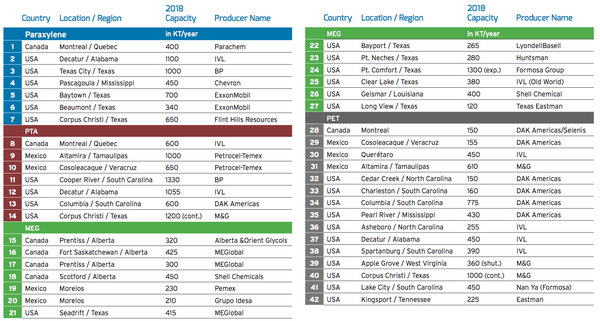

Perhaps the lack of imported PET used bottle bales from the USA and other regions due to National Sword could offer a lifeline to the smaller, less competitive plants in Asia. In 2016- 2017, 370 kt was imported to China and Hong Kong from the USA alone. That material must now be replaced by domestic production (Fig. 1).

What the table in fig. 1 does not show are some of the very creative scenarios for commanding large portions of the industry. For instance, Shell owns refineries and produces MEG, which means the company could also produce PX and then PTA. In the early 1990s, the company got into the PET resin business. If they had only then added PX and PTA, they could have dominated the entire value stream. Similarly, Amoco (now BP) had refineries PX, PTA and PIA, and even owned one of the original PET bottle manufacturing companies, but they opted to skip PET resin. Why didn’t they try PET? It could have been beautiful ...and well ahead of its time. Given BP’s ability to retain its huge margins in PTA for so many years, it is easy to believe that the PET industry would look much different today.

Chevron (refinery and PX) considered buying Eastman (PTA, PIA, PET, recycling) on two separate occasions.

Fig. 1: NAFTA PET Resin Industry Structure Evolution (source: SBAcci)

DuPont sent Dr. Malcom Smook out to travel the world looking for anyone and everyone who had ever made or bought a preform and who owned any type of blow molding machine. He was collecting royalties on every stretch blow molded PET bottle made before DuPont’s patent ran out in the late 1980’s. He was committed to capturing the value of Nathaniel Wyeth’s stretch-blow molded PET bottle patents. (Yes, Nate was indeed the brother of Andrew Wyeth – the famed American painter.)

DuPont re-entered the PET resin business for a short period – no doubt with a much broader secret business strategy that included making bottles. But it never materialized. In 1974, running short of cash, DuPont cancelled 21 large projects, including Corfam synthetic leather and PET bottles. They are just now selling off some of the remnants of those bigger and broader dreams with the sale of their PET film business to Indorama.

Speaking of Indorama, I visited the headquarters of Indorama in both Thailand and Indonesia in 1995. Mr. Lohia told me then that he would be a dominant global force, not just in polyester fiber, but in the entire PET business one day. At the time, I would have bet against it ... and I would have lost. I owe him a huge apology for my doubts. Today, no one doubts the brilliance of Indorama’s global strategy, their low-cost position, and their dominance.

For 18 happy years, the “Big Four” resin producers (Goodyear, Eastman, Rohm and Haas, Celanese) supplied the “Big Five” converters (Hoover Universal, Sewell Plastics, Continental Group, Owens-Illinois, and Amoco Container). These established converters would soon be joined by Plastipak Packaging, self-manufacturers at Carolina Canners, Western Container and Southeastern Container as well as a few more self-manufacturers and many, many other merchant container manufacturers.

But before these “Big Five” Coca-Cola was struggling with acrylonitrile bottles that literally popped under the pressure and the FDA began back pedaling on the acrylonitrile food contact regulation. Meanwhile, Pepsi-Cola was conducting initial trials with DuPont PET and test marketing their 32-fl. oz. bottle (this was long before metric volumes were used) with a snap-on base cup. Footed bases would not be commercialized by Continental’s crack technical arm for a few more years.

Amoco Container was the first to hit the market in 1977 with 64-fl. oz. PET commercial bottles produced at their Norcross, Georgia site and made of Goodyear PET. Goodyear beat Eastman and Celanese to the PET resin market because they could easily make relatively high IV1 PET bottle polymer thanks to their experience with solid-stating polyester tire cord. In contrast, Eastman, Celanese and Rohm & Haas were starting with fiber grade experience. The shift from 0.60 IV to 0.72 IV involved a more difficult learning curve than dropping from 1.0 IV to 0.80 IV. So difficult, in fact, that Eastman pushed 0.72 IV (Kodapak2 7352) for years before reluctantly making a 0.80 IV resin (Kodapak 9663). Even more time passed before the company

began making a 0.84 IV resin for the stress-cracking prone, one piece, petaloid3 carbonated soft drink bottle then being made by Continental. It was later made by their licensees Western Container, Southeastern Con- tainer, Apple Container and Tri- Coast Container. But solid state polycondensation (SSP) wasn’t the only issue holding Eastman back; Eastman was also still using DMT instead of PTA. Eastman did make the first green PET and first amber PET for beverage packaging, though. Getting colorants that satisfied the FDA and the technical requirements was not trivial and Eastman won that fight, only to give the value away.

What happened to the concept of using PET to diversify the aluminum can position (a strategy used by Continental Can, American Can, National Can, Ball, Crown Cork and Seal, and Heekin Can), or the strategy of diversifying the glass container business with PET containers, which was pursued by Owens- Illinois, Chattanooga Glass, and Ball-Foster. Shoot, O-I tried it twice, the final time with the acquisition of Continental PET Technologies, now GEC Packaging (Rank).

And don’t forget the long- standing feud between Hoover Universal and Sewell Plastics – the latter of which concentrated on HDPE extrusion blow molded milk jugs for the dairy industry before moving into PET. How

did that feud get started? Well, along comes Hoover Universal/Uniloy making EBM machines and selling them directly to the dairymen for self-manufacturing, thereby drastically reducing the market potential for Sewell.

So Sewell diversifies into PET, only to for their nemesis, Hoover Universal/ Uniloy entering the PET business. Sewell and Hoover Universal become fierce competitors again. Sewell sells out to what would become Constar, which was eventually sold by Crown Cork & Seal out of bankruptcy to Plastipak, but not before Amcor (formerly Hoover) made a valiant effort to purchase their old rival’s assets.

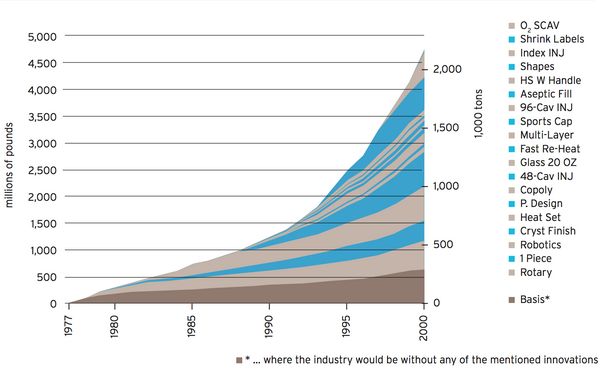

Fig. 2: Impact of PET innovation on consumption (source: SBAcci)

MUCH BAD BLOOD, MUCH DRAMA. JUST LIKE A REALITY TV SHOW.

The drama! After the non-compete expired, the Sewell family got back into the PET business with CKS (as in Charles K. Sewell) Plastics and now has a production facility in the original Sewell plastic plant.

An intriguing twist! After many business start-ups, failures, consolidations, mergers and acquisitions, the original “Big Five” converters are now back to the “Big Six” (Amcor, Plastipak, GEC, Coke, Pepsi, Nestlé).

We even have our celebrities. Charles K. Sewell, recent SPE Hall of Fame inductee, Elmer Sivacek; an associate of Lee Iacocca at Chrysler Defense brought into Johnson Controls to save their day; Gerry Kairins who still entertains his old employees at Continental PET Technologies with lavish, all expenses paid holiday parties, John Barth, the cigar chomping gutsy plant manager, who, after graduating from intense charm school with polish, became President of Johnson Controls’ Plastic Container division. Peter Weggeman, the forever-diplomat and President who led Continental’s diversification into the PET bottle industry. Dino Brownson who convinced Owens-Illinois to attempt PET containers for the second time, and for the fist time merged the brilliant minds at Continental PET and O-I. Dave Cornell, the horned-rimed glass wearing long- suffering champion of rPET and brightest technical mind mind in the PET recycling industry, and a current inductee into The Hall of Fame. T. J. Stevens who lead the Eastman IntegRex team out of the basement skunk-works to commercial success.

The three horsemen of PET chemistry at Dupont (Drs Bob Graham, Ross Lee, Jose Torradas), and many contemporaries like them at ICI in the U.K. doing early polyester chemistry research. Dr. Tom Brady, who pulled the brilliant minds of Frank Semersky, Bob Deardruff, Don Haywood, and Scott Steele out of O-I to form Plastic Technologies, Inc. Let’s not forget the entire Eastman Technical Service and Development lab under Robert Taylor, but especially Dr. Henry Gonzalez, on loan from Eastman R&D who single handedly solved the out-of- specification acetaldehyde challenge with his “1, 2, 3 Pellet” theory of AA generation in the injection molding machine; and let us not forget the contribution of Steve Zagarola at Coke who conceived the current AA specification knowing full well that it would make everything else in the PET bottle making process far better than we thought possible. Or the consistently challenging minds of Dr. Mark Rule of Container Science and of Dr. Greg Schmidt at BP; but perhaps none quite as influential late in the maturing PET industry as Guido Ghilsolfi.

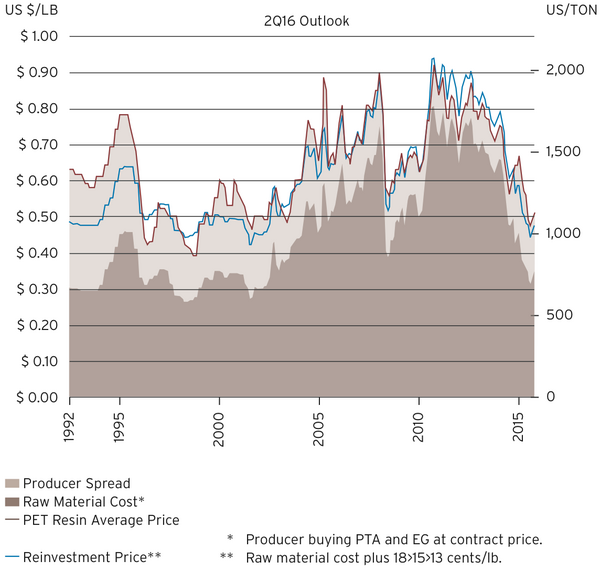

Fig. 3: USA PET producer spread (source: SBAcci)

CONVERTERS – HOW THEY HATE THAT TERM.

Converters – the term implies that all they do is generically convert resin to a finished product. The negative connotation is that converters are adding little to no value. Given that their margins are being squeezed by both resin producers and brand owners, both the name and the negative connotation seem fitting.

How do the converters break free from this paradigm? Consolidation has not worked as well as hoped. If converter margins get too sweet, then more self- manufacturing pops up (take Carolina Canners and Brunswick Container, to name just two). It’s a vicious cycle. A circular economy long before recyclers borrowed the term.

So, is innovation the answer? To fully appreciate the results of goal-focused innovation and development, a broad selection of seasoned industry professionals – including resin producers, equipment manufacturers, converters, bottlers, brand owners, closure manufacturers, and label producers – were surveyed back in 2000 to determine which innovation was responsible for the PET packaging industry’s growth from inception until the growth curve started showing the flattening typical of a maturing industry (Fig. 2).

Is there any drive left for advancing technology? Who is willing to fund it? Is it necessary? Instead of innovation, maybe the answer is simply to focus on cost. Lightweight the preform, and not just the body but also the base, the shoulder, the neck support ring and the thread finish. Make it a flexible bag with some type of fitment. Some water bottles are almost there already. Everyone likes to make fun of them, but consumers happily buy the least expensive bottles available, even if the physical performance is lacking. Brand owners have increasingly been unwilling to pay even the slightest premium to support R&D and innovation. They have instead been pushing these tasks onto converters and resin producers. Margins for raw material producers and resin producers have shrunk year after year (see Fig 3: USA PET producer spread chart).

This in turn forced reductions in technical staff and laboratories. Converters’ margins were also aggressively squeezed to compete with self-manufacturing. Eventually, there was no one left who was capable of innovative thought. Independent laboratories and development labs, such as Dev-Tech Labs (Amherst, New Hampshire), Plastic Technologies (Holland, Ohio), and a few others, flourished for years. Academic institutions, including Dr. Saleh Jabarin at the University of Toledo (Ohio), Michigan State University’s Packaging School and Clemson University’s Packaging Science department, attempted to fill the void. But they also struggle for funding and developmental direction from the industry.

Amid all of the distraction at the converter level, which still remains unsettled, the PET resin producing industry came to the realization that to conquer PET, one must understand PTA. With margins in PET resin being squeezed on both sides – PTA holding firm to their margins on the supply side, and the large converters and brand owners demanding lower prices on the buy side – a different business strategy for PET was needed.

What good is a PET resin plant without self-manufactured PTA? Given the speed at which the global polyester industry is learning, not much good at all. This answer may seem obvious now, but it was not so obvious to most for decades! Why did it take so long to recognize this fact? For a long time, other strategies were deemed more important and significant for improving margins. Take a look at the right side of the above chart (Fig. 1). The trend is toward large scale, melt- to-resin, acquisitions, expanding outside of NAFTA, private entrepreneurship, and ultimately complete raw material control if not outright ownership. Not just of PTA or MEG, but of both – and of ethylene and PX as well.

Resin producers who own these small plants and small lines (and this applies to all of them) are aggressively trying to find specialty materials to run on these stranded, smaller, and usually older and more costly assets. But the smallest of the older assets is still too large for any of the specialty materials (PETG wannabes) that have survived the gauntlet of manufacturing capabilities, new product introductions, test markets, market price pressures, consumer acceptance, and recycling hurdles. After all of these years, there are very few of these plants indeed.

(Note that Eastman held the PETG business and DID NOT sell it – e.g. the DMT, the CHDM, or the PETG assets – to DAK Americas 4).

How did PTA achieve such dominance over the PET producers? Many blame it on BP, but I think it stems from the fact that 85% of the PET molecule comes from PTA. Of course, BP also shares in the blame. BP maintained the perfect price-cost ratio making the decision to buy or make nearly impossible. Self-manufacturing your own PTA is both a huge capital commitment as well as a technical hurdle and an insurmountable patent wall. Anyone who did not begin self- manufacturing their own DMT or PTA purchased it from BP. In the early days, those who made PET with DMT were those who had an internal need for the methanol that is created as a byproduct (Eastman, DuPont, Celanese). Those who did not need methanol bought PTA from BP. Those who used both raw materials eventually stopped using DMT and converted to PTA.

What is the PTA self-manufacturing position now? Eastman makes all of their own PTA. DAK would be almost self- sufficient if they did not sell to their nearby competitors. They mostly purchase from Indorama in Canada and from BP for their plants in Mississippi and North and South Carolina.

Indorama purchased the BP PX and PTA assets adjacent to their new Alphapet plant plant in Decatur, Alabama. They also purchased the CEPSA PTA plant in Montreal that previously had close ties to Selenis. This occurred within a few months of DAK purchasing a controlling 50% interest in Selenis Canada. Why didn’t DAK buy the nearby CEPSA PTA plant? This is a great question. The answer comes down to logistical reasons and the complicated dynamics of supply and demand.

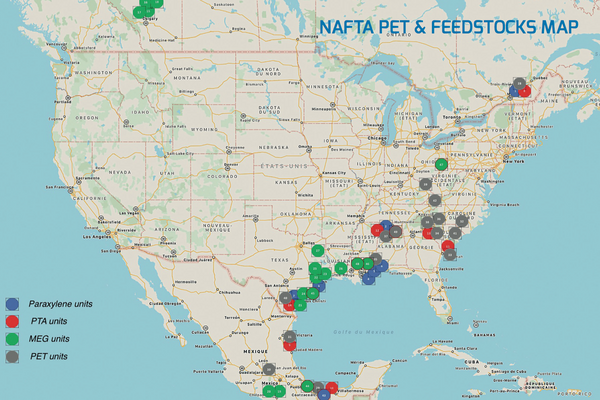

If you look at map of all of these PTA and PET facilities, you would hope (and rightly so) that even competitors could work out a swap arrangement for PTA to avoid all of the unnecessary freight.

Those that fail to integrate will not survive. M&G was desperately trying to get there. The finish line was in sight. They were oh so close.

One might ask why BP would not opt to keep their customers more competitive with self-manufactured PTA? From a business perspective, why should they? They have set a limit to their willingness to forgo profits in order to maintain market share. So, profits will remain ... until the customers are gone. BP proved their commitment to this strategy with M&G in the US and with JBF in Belgium.

Healthier PET producers continue to pursue backward integration – not just with PTA, but also with PX and maybe even further back in the supply chain (MX, refinery, crackers?). Indorama are back into PX and ethylene. Guido Ghisolfi carried a folder around simply labeled “REFORMER”. I never got a peek inside. Maybe it was just an empty folder used to bluff his raw material suppliers. I prefer to believe that perhaps, as early as 1995 Guido realized the importance of backward integration and had already analyzed the FULLY integrated PET plant – integrated all the way back to a refinery. What better location to fulfill that dream than in Corpus Christi, Texas? So close ... just 90 more days ...

Now that we are 90 days post-bankruptcy for M&G in the US, we are starting to see some clarity. Far Eastern New Century submitted the winning bid for M&G’s Apple Grove PET resin plant. There appear to be multiple parties interested in the Corpus Christi construction site. We should know who the future owners will be once bidding closes in March for Corpus Christi.

But through all of this, we cannot count M&G out. As of this writing, they are producing PET in Altamira. They are developing new strategies and new relationships. Have we seen the end-game for M&G? I think not.

Apple Grove is a good financial decision at least for the short term until excess capacity comes back to the NAFTA market with Corpus Christi or Alphapet 2.

So why the interest? Specialty materials? This also seems unlikely – there’s not enough of a market. What about a new NAFTA-based foothold for those who have been kicked out of the US market as a result of antidumping or countervailing duties, or both? Ahh, that’s the answer.

With Corpus Christi still available, that would narrow it down to someone from Oman, India or China kicked out as the result of ADD & CVD 1.0. And now possibly Taiwan, Indonesia, or Korea if they believe that they will be kicked out as the result of ADD and CVD 2.0.

If any of these new, non-NAFTA producers come to America (and FENC already has), the cycle will start again. New players, new strategies, new partnerships, and retribution from the buyers to the legacy producers. Drama will return, but this time it will look more like chaos. Buyers love chaos and excess capacity. Margins will suffer. Businesses will suffer. Plants will close. Consultants will remain very busy.

But don’t let the entertainment factor distract you. From now until late-2018, there will NOT be enough PET capacity in NAFTA to go around. In the immortal words of Bob Ayres at Western Container, “Running out takes all the fun out of buying cheap.”

Spot prices are trending up, way up! Purchases are being made in the strangest ways from the strangest sources. Specifications and qualifications are not as important as they were 90 days ago. 90 days. M&G was close ... oh so close.

The comPETence center provides your organisation with a dynamic, cost effective way to promote your products and services.

magazine

Find our premium articles, interviews, reports and more

in 3 issues in 2026.