In this piece, we will first review the global consumer packaging industry in light of sustainability pressures, central to the wider plastics packaging industry and to PET. We will secondly examine PET bottle performance, market dynamics and opportunities within lead end-uses for PET, consider the value that remains placed on PET as a lightweight, convenient and sustainable format, the latter if it is handled correctly.

Sustainability is the key for plastic packaging.

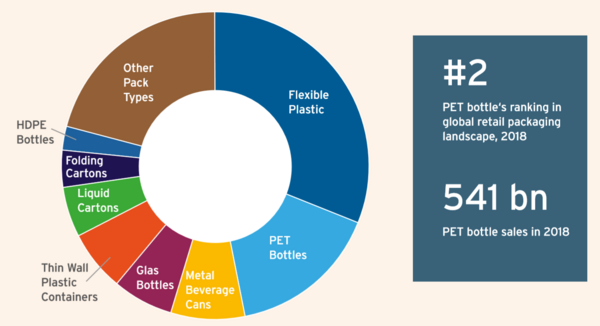

While many will rightly attest to sustainability having long been a trend for the consumer packaging industry, there is absolutely no doubt as to this trend’s more critical standing today, requiring urgent attention. This is driven by public scrutiny and legislative/NGO pressures for action on the plastic waste polluting the world’s oceans and land environment, thereby making plastic, including PET, the in-focus packaging material. Plasticdominated substrates accounted for 63% of global retail packaging sales in 2018.

There is a far heightened momentum now throughout the value chain to advance and improve via sustainable packaging solutions, also widely apparent within soft drinks, the leading industry enduse for the PET bottle. Research is being undertaken, solutions developed, proposed and requirements being made by brand owners and retailers, as users of packaging, to evolve offerings and address concerns about what are seen as “single-use plastic pollutants”. Sources, including the European Commission, for example, cite that two thirds of plastic waste in Europe comes from packaging.

Advances are being made on recovery and reuse but this varies widely by country as do rates of consumer recycling. Governments and NGOs are increasingly making clear the need for sustainable packaging as part of the solution to safeguard the health of the planet. Consumers play a role to drive this need. “I want a plastic-free world” is one of Euromonitor International’s top 10 global consumer trends in 2019. The desire for a plastic-free world is largely consumer-led and will gain momentum. However, as the conversation evolves, the understanding of plastics’ value will likely grow too, and the emphasis will increasingly be placed on responsible use and focus on waste.

Fig 1: Global Leading Packaging Formats 2018 (Source: Euromonitor International)

It is clear that sustainability is becoming much more than a nice-to-have but an expectation among a rising number of consumers and brands across the world.

As such, since the pivotal turning point of end 2017/early 2018, commensurate with a wider public awareness of plastic pollution - resultant of the Blue Planeteffect, the launch of the European Plastics Strategy, China’s ban on waste, media attention and corporate players’ pledges on packaging recovery among other initiatives - here we are, almost two years on and can witness a movement gravitating towards a circular economy. From brand packaging design through to recovery and onward re-use, initiatives to improve handling of plastic and reduce reliance on petroleum-based plastics, are growing. With this movement comes change, opportunity and innovation.

Remove, return, re-use and refill strategies

For the drinks industry, leading end-use for PET bottles, altering the consumer purchasing culture to one of return postuse, such as via a deposit-return scheme (DRS), can aid plastics recovery and reduce waste; countries such as Germany and Norway exemplify the high recovery possible using a DRS. Discussions examining the possibilities of adopting such a system in the UK, continue.

There are a number of refill packaging solutions, outside the core arena of drinks, which encourage return and re-use. The Loop re-use e-commerce model, one recent example, is currently being trialled and backed by a number of fast-moving consumer goods leaders, such as PepsiCo, Unilever and Nestlé. Among brick-andmortar grocery stores, a re-thinking of packaging via removal and reduction is similarly apparent. Packaging-free, plastic-free and zero-waste concepts may be niche but they are growing. Early June 2019 has seen UK retailer, Waitrose & Partners, launch an 11-week trial at one of its stores in Oxford, offering unpackaged fruit and vegetables and refill stations for a number of foods, for detergents, beer and wine. This trial has been extended following positive consumer response.

Fig 2: “Waitrose Unpacked” trial of refillables in the UK

rPET in high demand

The soft drinks industry accounted for 88% of global PET bottle sales in 2018. PET is broadly highly recyclable but further to this there is a heightened demand for recycled PET (rPET), a clear brand response that illustrates a plastic re-use solution in action as brands, retailers, packagers and recyclers seek to remove the negative “single-use” association with soft drinks retailed in PET bottles.

There is a clear need and urgency to advance on recovery, to fuel greater re-use and enable PET much more than one life span. Countries such as Germany, Norway and Japan execute well on collection, recovery and recycling of plastic. Improved recovery rates of PET across countries and across municipalities within countries indicate a need to harmonise and so make recovery more achievable and advance its re-use in packaging, as via rPET, to ultimately reduce the volume of plastic waste ending up in the environment.

Fig 3: Cross-FMCG “Loop” trial of re-usable, refillable packaging

There is a commercial benefit, to meet the rising demand for rPET where the greyness of recycled polymer content is less balked at, it can even be a marketing aesthetic, evident among some soft drinks and beauty brands, to communicate to consumers the brand packaging’s recycled content and onward recyclability. Brands are showing how they seek to deliver on their plastic packaging commitments regarding recovery, recycling and onward re-use of plastic through incorporating recycled plastic content in their PET bottles.

Summer 2019 has seen global brand leader in bottled water, Nestlé SA in Europe, transition their leading Belgian brand, Valvert to 100% rPET bottles and advance recycled content in its Aquarel brand alongside a myriad of other updates with varying levels of rPET content. They are not alone, increases interest in rPET is evident across brands and private label ranges.

Round-Up of Global PET Bottle Demand in 2019 and Core Performances

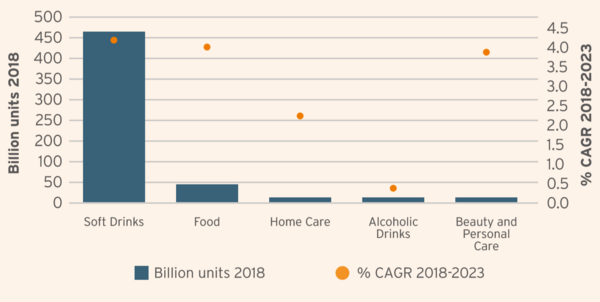

The PET bottle is virtually ubiquitous across many of the soft drinks categories with global demand led by bottled water, carbonated soft drinks and ready-to

recovery drink tea. As such, the PET bottle holds a prominent presence in the global grocery channel, ranked as second most commonly purchased consumer pack type, accounting for 15% of global retail packaged goods sales, second only to flexible plastic, in 2018 volume sales.

Fig 5: Global PET Bottles by Industrie End-use in 2018 and Forecast Growth (Source: Euromonitor International‘s Passport Packaging system)

PET by Industry Snapshot: Leadership in Soft Drinks

We forecast a healthy 3.9% rise in demand for PET bottles in 2019, even within this climate of concern regarding sustainability. Growth is indicative of healthier drinking habits across the world, particularly favouring the purchase of bottled water and water-like beverages. Asia is of greatest regional importance to deliver growth for PET.

Europe’s demand for PET amounts to 112 billion bottles is sizeable and growing; Western Europe is characterised by more mature markets and well-developed single-serve bottles sales, with onward opportunity for single-serve PET bottle growth for soft drinks in the Eastern part of the region. It is not all growth for the PET bottle in Europe, in alcoholic drinks, the PET bottle records decline in Eastern Europe; this primarily relates to faltering beer consumption in Russia impacted by continuing economic instability and sanctions to restrict alcohol consumption and address alcoholism in the country.

Preference for PET in bottled water; health and rPET are primary growth drivers

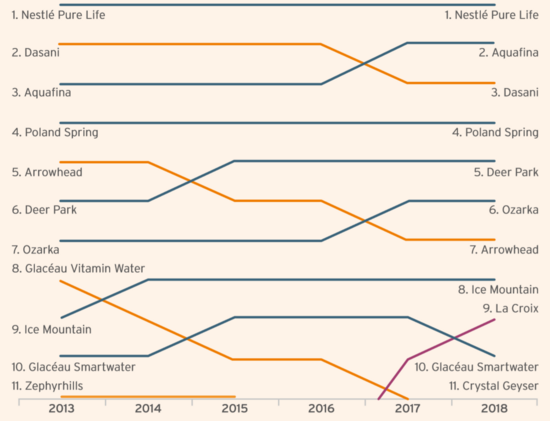

In bottled water, the PET bottle is the go-to pack format faring well with expanding demand for on-the-go formats as sub-1-litre bottles record strongest sales growth. Added to this is the significance of bottled water to overall soft drinks consumption, standing at 49% of litres of soft drinks consumed in 2018 and rising. The sugar reduction pre-occupation of consumers in North America explains bottled water growth as high sugar content CSDs and juices witness declining sales in the face of sugar taxes and even bans on sweetened beverages in certain areas, raising awareness of the implications posed by sugary drinks, Flavoured water is a star performer among US consumers with brands such as LaCroix, notably sold in beverage cans akin to carbonates, enjoying rapid sales growth as healthy alternatives to other soft drinks, enabling LaCroix to enter the top 10 bottled water brands in North America, in 2018. As US consumers are clearly showing a taste for carbonated, flavoured, unsweetened waters, private label offerings are further enjoying growth and growing this category.

Asia Pacific holds strongest volume prospects for bottled water; this region alone is set to account for more than half of global forecast volume growth for PET bottles in the category over 2018-2023, led by rising demand from consumers in China, India and Indonesia. For China, conversion from less healthy soft drinks also rings true for bottled water’s development as does consumer concern over tap water quality.

Fig 6: Bottled Water in North America: Top 10 Brand Rankings 2013-2018 (Source: Euromonitor International‘s Passport Packaging system)

In Europe, Italy leads bottled water consumption in PET bottles, at over nine billion bottles sold in 2018, Spain is another highlight, set to lead onward volume growth for PET bottled water in the region; Spain’s economic recovery and the broader wellness trend support growth of the dominant still bottled water with dynamic opportunities presented in smaller end-uses of carbonated and flavoured waters; consumers’ health-consciousness again at play as the shift from the traditional carbonated soft drink continues. Investment in production capacity to meet rising consumer demand for bottled water is apparent (including by Calidad Pascual, Aguas Font Vella y Lanjaron and Agua Mineral San Benedetto)

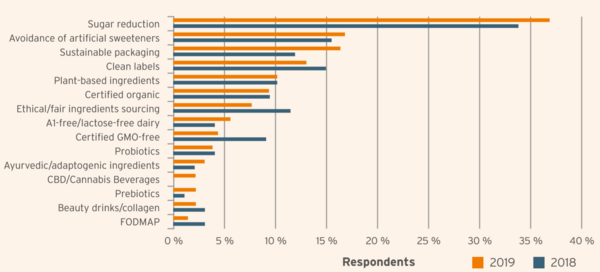

Per results of Euromonitor’s latest Voice of the Industry survey for Non-Alcoholic Drinks, consumers’ health-consciousness is clearly pinpointed as lead driver for soft drinks development, evidenced by the rising importance placed both on “sugar reduction” and “avoidance of artificial sweeteners”, the top two “extremely influential” trends for 2019.

In Spain, flavoured water organic entrant from Font Vella and Vichy Catalan Fruit, variant sweetened with stevia from Vichy Catalan in Spain, both respond to these trends.

Fig 7: “Extremely influential“ Trends in Non-Alcoholic Drinks - 2019 vs 2018 (Source: Euromonitor International Non-alcoholic drinks Voice of the Industry survey, May 2019)

Carbonated soft drinks? Clearly challenged by the advance of water but there are value-add opportunities

In carbonated soft drinks, value sales interestingly outperform litre volume consumption rates, indicative of an increase in price per litre spend, part of this being a premiumisation trend as value-add carbonate offerings that have a natural/botanicals leaning perform well and seek to address wellness concerns with more natural options. Increased price per litre comes also as a result of a growing implementation of sugar taxation across countries, the consequent rise in smaller sizes being seen and reduced sugar variants, both for single-serve and family multi-serve packs, to keep retail unit prices affordable.

Table: Global Carbonates Volume vs Value Growth 2017-2018

- Litre Volume: 0.2%

- PET Bottle Unit Volume: 1.6%

- USD Value: 2%

In volume sales for PET, Asia Pacific remains number one region for performance and growth: Philippines, China and South Africa leading volume gains for PET bottles in the category over 2013-2018 while North America is the weakest, the result of a consumer shift to “healthier” alternatives - water and RTD tea leading the way.

PET, however, has competition because of the rise in zero-calorie variants and premium sparkling (such as botanicals) with product innovation in adult mixers enabling glass to enjoy a return to growth in carbonates, which has been in decline for several years. Brand Fever-Tree extended its botanical range of mixers with “lighter” variants addressing premium and health needs, designed as a companion to a premium spirit and as a premium nonalcoholic drink to consume on its own, especially popular among millennials, serving to add to the packaging growth dynamics in this challenging category. In spring 2019, Coca-Cola introduced its range of four mixers designed to partner with dark spirits, retailed in a premium, heritage glass bottle.

Beverage cans too, in smaller sizes, show improving sales with slimline sleek designs and brand launches linked to craft, premium and natural trends, sparking pack design innovation.

Fig 8: Bottled Water in North America: Top 10 Brand Rankings 2013-2018 (Source: Euromonitor International‘s Passport Packaging system)

Prospects in premium functional beverages, dairy and non-dairy products

Beyond the lead soft drinks end-uses of water and carbonates, PET bottles benefit from category blurring and expansion of wellness beverages. In juices, while decline has occurred, as evident in North America and Europe, also children’s juice drinks related to sugar concerns in many markets, opportunities lie in portioning, in offering premium functional juices that focus on nutrients and health benefits, in small packaging.

Beverages that go beyond the important hydration-giving properties of water can additionally expand category growth - beverages that compete as preventative health tonics, probiotics or are beauty positioned, for example beverages designed for skin health as part of the “beauty from within” trend - and command a premium price point. Veganism and vegetarianism promotes scope for growth in dairy and non-dairy drinks. Fibre and protein-rich plantbased dairy alternatives show a growing traction via nut, grain and pulse options with an array of coconut, almond and oat milks joining the retail shelf.

Final words

PET holds leadership position in rigid plastic with strong category performance driven by consumers’ healthy living and hydration preferences spurring on global consumption of bottled water and water-like beverages with growth prospects also for functional beverages.

Integral role to PET’s onward role and perception, is the industry’s action together in collaboration with brands, retailers, governments, recyclers, consumers, the entire value chain, to innovate and advance most urgently on packaging recovery and re-use with sustainability at the heart of development and so address plastic waste.

PET already has the widespread advantage of recyclability across many of its enduses, however advancement on circularity is crucial. 2025 is a targeted timeline for many on plastic packaging recovery and recyclability. Corporate players in the value chain that do not adapt and integrate sustainability into their practices may come under more pressure as consumers’ awareness and concern surrounding the environment elevates, influencing their purchasing decisions.

The comPETence center provides your organisation with a dynamic, cost effective way to promote your products and services.

magazine

Find our premium articles, interviews, reports and more

in 3 issues in 2026.