In this new edition of comPETence, Euromonitor International explores the key opportunities for growth, but also the challenges that await PET bottles in the core beverage industry to 2019. In the key soft drinks market, packaging downsizing should enable PET to meet consumers’ desire for convenient, ‘calorie’ sized bottles; better address children’s consumption, and allow brand owners to add value to their offering. Changing legislation and premiumisation in alcoholic drinks will present a challenge for the pack type to gain a foothold.

Amid high saturation levels, PET benefits from key position in basic categories

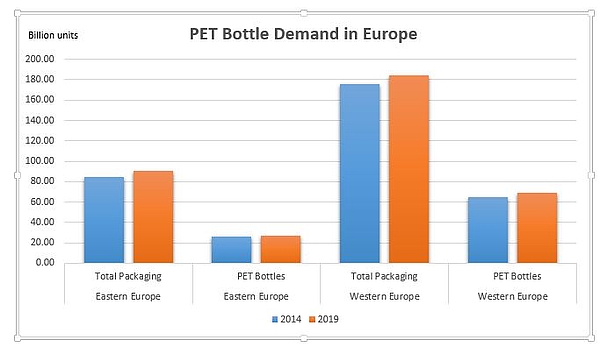

PET bottles stand in second position in the overall retail packaging landscape in Europe, representing 104.1 billion units in 2015. PET’s leading position is only outperformed by flexible plastic, which is significant in packaged food as basic packaging for indulgence products such as confectionery, biscuits, and baked goods, as well as staples like processed meat, cheese and rice.

PET bottles also benefit from a privileged position within primary need products. Almost 88% of PET volume sales stem from the beverage industry in Europe; 83% made up by soft drinks alone. When considering how savvy European consumers have become since the global economic downturn of 2008-2013, achieving and maintaining this position in basic products is essential to the future success of PET in the region.

In soft drinks, smaller PET bottles to fit well in fight against sugar intake

In fact, the European consumer, particularly the Western European consumer, more than ever perceives its soft drink product as a necessity; a means to remain ‘operational’, active and healthy. This is why in bottled water, PET’s largest category by far at 49 billion units in 2015, a shift towards smaller pack sizes is evident. Greater portability of a bottle means its end user can easily re-hydrate while on the move, at any time of the day. The 500ml PET bottle format is expected to yield the highest volume growth over 2015-2019 with 580 million extra units to be sold. That is more than the 1.5-litre and 1-litre alternatives that remain more suitable for home consumption. This added convenience is being increasingly aimed at children, with new water brands being made available in smaller sizes in 2015, such as Highland Spring in the UK and Morshynska Sportyk in Ukraine. Both brands offer a 330ml PET bottle fitted with a flip-top closure.

It is a similar story in juice, with 200ml children’s lunchbox format bottles performing best. With legislative discussions at EU level increasingly pushing food and soft drinks brand owners to reduce sugar content in their products, the pack size will remain one way to suggest a lower intake of calories to shoppers. PET will however, face competition from pack type alternatives, such as shaped liquid cartons as used by the Vita Coco brand of coconut water for example, or aluminium/plastic pouches as per Capri-Sun in juice drinks.

Within this context, carbonates is arguably the category presenting the biggest challenge in soft drinks in Europe. The second largest category for PET with 26.9 billion units, boasts a positive yet low CAGR of 0.7% over 2015-2019. Packaging volumes, which includes a large share for metal beverage cans, are just about managing to maintain growth in Europe; one way to ensure the sustainability of this trend going forward is to further promote small pack sizes, such as 330ml, as a way to address consumer concerns over calorie intake. This on-the-go pack size offering still has further potential for growth in Eastern Europe. Although beverage cans remain behind in volume terms, PET may also benefit from a design revamp in order to ensure a more premium look is conveyed and to fit with any ‘better for you’ product claim.

Wins in alcoholic drinks hampered by premiumisation and packaging legislation

PET bottles record much lower volumes in alcoholic drinks, representing only 4% of total retail packaging in Europe. Although the pack type does have options to gain presence, these remain fairly small in volume terms and the industry entails some real challenges. Overall packaging demand is expected to go up by a shy CAGR 0.5% to 2019 in the region. While Western Europeans’ health preoccupations result in them drinking less but better quality and therefore to seek more pack solutions like glass bottles, Eastern Europe’s slow growth in alcoholic drinks consumption is to a good extent due to the Russian government’s strong anti-alcohol policy; not unlike some of the laws previously passed by the Turkish authorities.

Consumers’ cautious behaviour in Western Europe is particularly visible in Germany where packaging unit volume sales are likely to see a noticeable decline to 2019. At the same time, craft beer is becoming more and more popular, with the quality promise and local provenance often acting as real USPs. The craft beer trend should benefit glass bottles and possibly also beverage cans; whilst PET will remain a more mass and economy alternative. PET bottles should nonetheless make interesting headway in the UK in the dynamic cider/perry and still light grape wine categories. Both categories in the UK are undergoing a general diversification in packaging formats; with PET mainly serving the economy platform and in large sizes such as 2-litres for cider/perry, and seasonal consumption with single-serve 250ml bottles.

Legislative changes in Russia are shaking PET’s unique position in alcoholic drinks in Eastern Europe. In 2014 the Russian government, in a bid to prevent alcohol from being too affordable, proposed a ban on PET bottles that are larger than 500ml for beer and other alcoholic beverages; though this has not yet come into force. This could come as an additional obstacle to PET growth in alcoholic drinks after Turkey ruled in 2012, that plastic packaging would be banned for alcoholic drinks, with the exception of beer. PET will however still continue to gain ground in neighbouring countries such as Romania where local positioning and economy sizes, such as 2-litres, are still very much favoured by beer drinkers.

PET bottles are expected to generally overcome difficulties pertaining to tight economic conditions and health concerns. Over 2015-2019 the pack type is due to increase by some 5.7 billion extra units in the European retail packaging landscape. Using a pack sizing strategy in order to align with changing consumer behaviour will however remain key for PET to maintain its leading position in soft drinks as well as in winning new markets.

In upcoming issues of comPETence, we will continue to examine some of the brand initiatives and trends for PET bottles taking place in other world regions.

The comPETence center provides your organisation with a dynamic, cost effective way to promote your products and services.

magazine

Find our premium articles, interviews, reports and more

in 3 issues in 2026.