Regulation has disconnected prices of packaging suitable grades of recycled material from:

- virgin values

- grades primarily serving other end-uses

- feedstock costs.

This a pattern repeatedly shown through analysis of the yearly average price spreads against virgin and feedstocks across recycled polyethylene terephthalate (R-PET), recycled high density polyethylene (R-HDPE) and recycled polypropylene (R-PP) markets.

These are the types of spreads featured in ICIS’ new Circular Plastics supply, demand and pricing beta (alongside long-term supply & demand data and forecasts). The beta is accessible via a short questionnaire here.

There are two key events that show the impact most clearly:

- The 2019 entry into force of the EU’s Single Use Plastics Directive (SUPD)

- This included mandatory 25% recycled content targets for polyethylene terephthalate (PET) bottles by 2025, and 30% recycled content targets in all plastic bottles by 2030

- Individual countries then had until 2021 to fully translate the SUPD into national law

The 2022 publication of the draft Packaging and Packaging Waste Regulation (PPWR)

- This entered into force in January 2025 and included mandatory recycled content targets across most plastic packaging

- It replaced the previous Packaging and Packaging Waste Directive (PPWD)

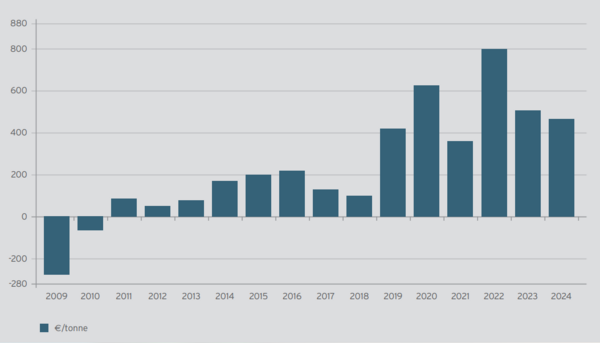

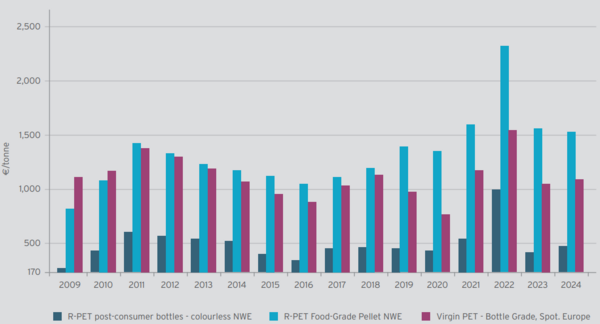

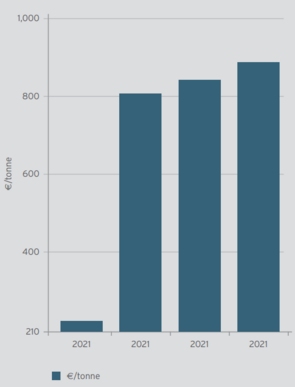

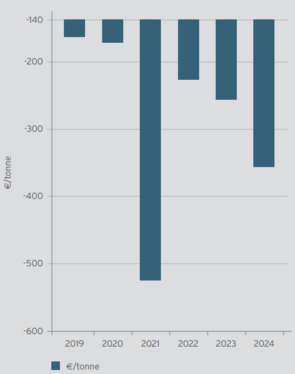

Recycled polyethylene terephthalate (R-PET) food-grade pellets (which predominantly serve the bottle-to-bottle market) have traded at a premium to virgin PET bottle grade spot prices on average yearly basis since 2011.

The variation in the average yearly spread has intensified in recent years, suggesting increased decoupling between the two markets.

Nevertheless, since the entry in to force of the SUPD in 2019 there has been a marked increase in the spread compared with all prior years, as shown in the below bar-chart.

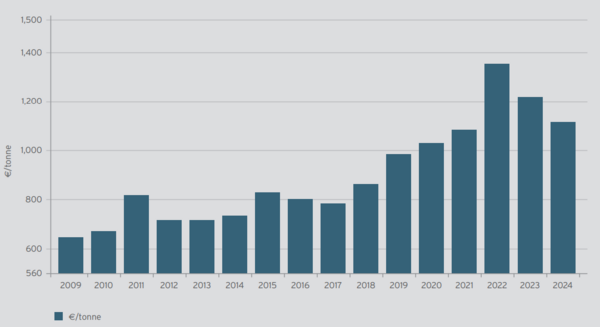

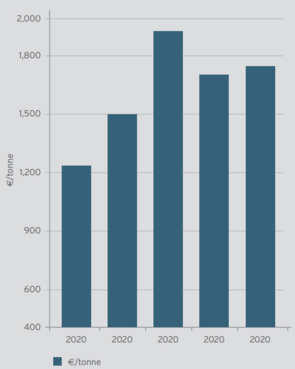

A similar – but less pronounced trend can be seen in the premium between R-PET food-grade pellets and feedstock colourless post-consumer PET bales, whereby the spread in each year from 2019 onwards remains higher than any year prior to 2019.

Meanwhile, yearly average prices for R-PET foodgrade pellets in each year since 2021 (the deadline for fully translating the SUPD into national law) have been consistently above any year prior to 2021. 2011 was the only prior year that saw higher average yearly prices than 2019 and 2020.

2011 saw what were record high prices at the time throughout the R-PET chain, in part attributable to a swathe of sustainability initiatives from brand owners.

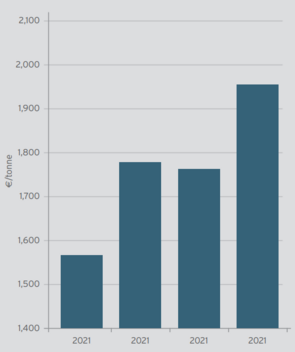

While 2023 and 2024 saw challenging macroeconomic conditions, yearly average R-PET prices remained consistent with their 2021 level (coming back from 2022 record highs driven by bale shortages and voluntary sustainability targets).

Spreads with feedstock meanwhile in both 2023 and 2024 were above any year prior to 2022 (although production costs were also higher as a result of the energy cost crisis), and spreads with virgin higher than any year prior to 2020. Turning to recycled high density polyethylene (R-HDPE) and similar trends can be seen in the wake of the publishing of the first draft of the PPWR by the EU Commission in 2022.

This was the first point where the general market became aware of the scope of the minimum recycled content targets.

The average yearly spread between blow-moulding R-HDPE pellets (which predominantly serves packaging) and virgin blow-moulding spot prices has been at least €347/tonne higher than the years prior to 2022 in every year from 2022 onwards.

For natural post-consumer R-PP pellets each year from 2022 onwards has seen the spread with virgin at least €567/tonne above 2021 levels.

The average yearly spread between R-HDPE blow-moulding pellets and feedstock mixedcoloured bales, meanwhile, has been at least €263/ tonne higher in each year from 2022 than the years preceding it.

R-PP natural post-consumer pellets have seen a spread with feedstock mixed-coloured bales of at least €190/tonne higher than 2021 in each year from 2022 onwards.

_______________________________

''While 2023 and 2024 saw challenging macroeconomic conditions, yearly average R-PET prices remained consistent with their 2021 level (coming back from 2022 record highs driven by bale shortages and voluntary sustainability targets).'' - ICIS

_______________________________

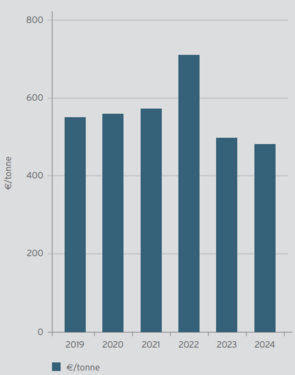

Taken together, the ‘break points’ that legislation creates in the market are clear. Comparing the trends in non-packaging grades makes this even starker R-HDPE pipe-grade pellets provides the clearest example, but the trends are similar across other non-packaging grades in Europe.

As the name suggests R-HDPE pipe-grade pellets serve the pipe industry rather than packaging.

Players in this sector typically purchase based on cost-saving against virgin, and the pipe sector is heavily linked to construction demand where there are no current regulatory targets on recycled content that have been proposed in the EU.

The yearly average spread between pipe-grade black and feedstock bale costs reached fresh record lows in both 2023 and 2024.

Meanwhile, the yearly average spread with virgin shows that black pipe-grade pellets have become progressively cheaper compared with virgin injection moulding spot prices in both 2023 and 2024.

The lack of regulation has meant that pipe-grade black pellets have been more exposed by the negative impact of the cost of living and energy cost crises on the construction sector, while regulation on packaging has acted as a bulwark, comparatively.

The change in the spread with feedstock comes at a time when production costs have increased.

For recycled polyolefins the conversion cost between bale to pellets is currently estimated at €400-500/ tonne, up from an estimated €300/tonne before the current inflationary cycle.

This has meant that in 2023 and 2024 many players have struggled with margins, and in some cases players have been selling at a loss.

Technical limitations mean that the bulk of material across recycled polyolefins serves non-packaging rather than packaging markets – and the majority of producers serving packaging sectors also serve non-packaging sectors. So while on the face of it margins on packaging grades may seem high, it does not demonstrate the health of the overall industry.

Consolidation risk in the market was high in both 2023 and 2024, and remains so in 2025. Squeezed margins on non-packaging grades are also limiting recyclers and waste managers’ ability to invest in additional sorting, infrastructure and production capacity necessary to meet EU recycled content target.

The data clearly shows that regulation does have an impact. It also shows that when unevenly applied it can add market fragmentation, distortion and complexity that can harm the achievability of its goals.

The comPETence center provides your organisation with a dynamic, cost effective way to promote your products and services.

magazine

Find our premium articles, interviews, reports and more

in 3 issues in 2026.